Why battery costs have plunged 89 percent since 2010

Why battery costs have plunged 89 percent since 2010

A 600-fold increase in battery production made batteries much cheaper.

{kind=link}

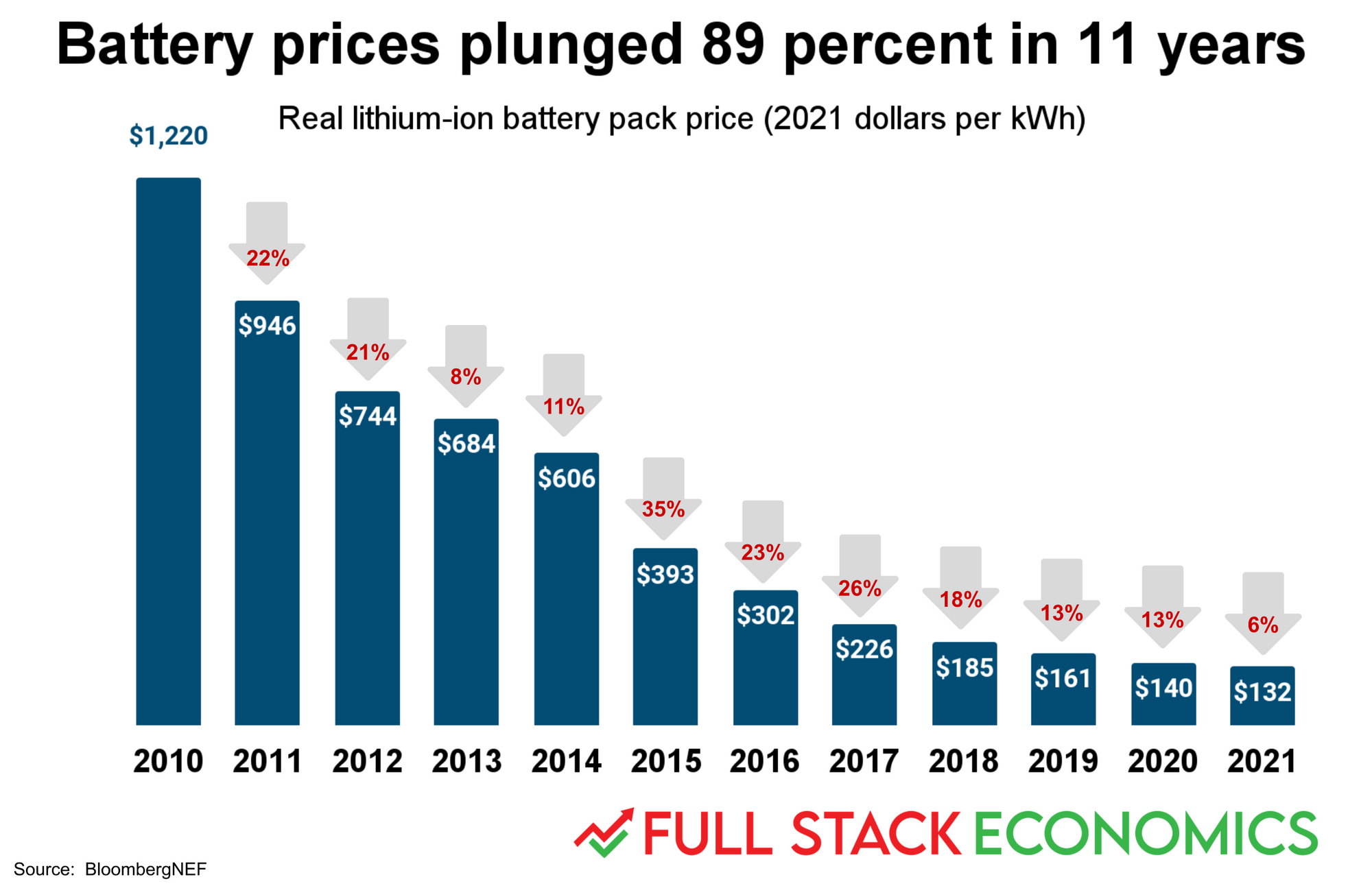

The average cost of lithium-ion batteries used in electric cars and other products fell by 6 percent (adjusted for inflation) since last year. Since 2010, these costs have declined by an amazing 89 percent. That’s according to a new report by BloombergNEF.

Due to rising commodity prices, this year’s 6 percent decline is actually the smallest since 2010. And the report warns that battery prices may actually rise next year.

But BloombergNEF remains bullish over the longer term. From today’s price of $132 per kilowatt-hour, lithium ion battery packs are projected to fall below $100 by 2024 and $60 by 2030.

Cheap and reliable batteries will be essential for decarbonizing multiple industries.

Until recently, the high cost of batteries made battery-electric vehicles (BEVs) much more expensive than conventional gasoline-powered cars. But when batteries cost less than $100 per kWh, unsubsidized BEVs will start to be cheaper than conventional cars. At that point, BEVs could start to rapidly gain market share from conventional cars.

Battery costs are also a key obstacle to decarbonizing the electric grid. Solar panels and windmills have gotten dramatically cheaper over the last decade. But neither technology works 24/7. So we’ll need a way to store power for times when it’s not sunny or windy. Lithium-ion batteries aren’t yet cheap enough to do this profitably. But they are getting closer.

So the potential benefits from cheaper batteries are massive. And there’s good reason to expect battery costs to continue falling for years to come.

Economists have found that manufacturing costs often decline at a predictable rate. In a model known as an experience curve, costs fall by the same percentage (called the learning rate) each time industry-wide volume doubles. This model has fit the battery industry well, and BloombergNEF estimates that the learning rate for lithium-ion batteries is about 18 percent.

The global battery industry has already grown massively: output rose by a factor of about 600 between 2010 and 2021. Costs fell by 89 percent as a result. But there’s still a lot of room for further growth: few people own electric cars, and grid storage technology is still in its infancy. As these sectors expand, prices should drop further.

How Tesla pushed down battery costs

Let’s go back to 2003, the year Tesla was founded. At the time, lithium-ion batteries were primarily used in laptops and cell phones. Tesla’s founders realized the cost and performance of these batteries had gotten close to the point where a few thousand smartphone batteries could power a commercially viable electric sports car.

Back then there were already hundreds of millions of laptops and cell phones being sold every year. Electric cars sell in much smaller numbers than that, even today. However, a single electric car needs thousands of times more battery capacity than a smartphone. So as Tesla ramped up production during the 2010s, it quickly became one of the world’s biggest battery buyers.

Indeed, Tesla’s appetite for battery capacity was so large that in 2014 it announced plans to build its own “gigafactory” in partnership with battery maker Panasonic. The Nevada facility was designed to eventually produce 35 GWh of battery cells per year—enough capacity to supply hundreds of thousands of electric vehicles annually.

It wasn’t initially obvious that Tesla could build enough vehicles to keep the factory busy. So Tesla branched out into energy storage products. In 2015, Tesla unveiled a wall-mounted battery called the Powerwall that allows a home to remain powered during an outage. Not long after that, Tesla started building massive battery installations to help electric utilities manage their power grids. An early installation in California offered 80 MWh of storage capacity—comparable to roughly 1,000 Tesla cars or a few million iPhones.

In a 2014 talk, Tesla CTO JD Straubel explained how the scale of the Gigafactory would help Tesla bring down its battery costs:

We're going far upstream in the cell manufacturing process. We're not just looking at how do we do a winding of a cathode or anode better, but we're looking at coating, we're looking at the material synthesis to build the cathode and anode, we're actually going all the way back to literally some of the places where the raw materials come from. If you start breaking down the cost and build a big pie chart of what's driving cost on a lithium-ion battery today, materials are actually a reasonable part of that. But even those material prices can be reduced if you drive the right volume and drive purchasing power into how you're buying them.

Not only does a battery factory benefit from economies of scale, most of a factory’s suppliers can enjoy economies of scale if they get sufficiently large and predictable orders. As the world’s largest electric carmaker for the last decade, Tesla has been able to place bigger orders than almost anyone else for batteries and the raw materials that go into producing them. And as a result, it has enjoyed some of the lowest prices in the industry.

New battery chemistries bring down costs too

The term “lithium ion battery” actually encompasses a range of battery designs that combine lithium with other elements like iron, nickel, or cobalt in various combinations.

BloombergNEF reports that Tesla’s favorite battery technology in recent years uses nickel, cobalt, and aluminum oxide (NCA). Over time Tesla and Panasonic have worked to replace the expensive cobalt in their batteries with cheap nickel. According to BloombergNEF, NCA batteries were about 80 percent nickel when they were first introduced in 2012. By 2020, the nickel content was up to 90 percent. Panasonic is aiming to completely remove cobalt from these batteries by 2024, yielding a design that is 95 percent nickel.

At the same time, Tesla has started using another battery chemistry called lithium iron phosphate (LFP) in some of its vehicles. Iron is one of the cheapest metals around, so LFP batteries tend to be significantly cheaper than NCA batteries. Current LFP batteries have lower energy densities than NCA batteries, making them unattractive for Tesla’s high-end vehicles but adequate for entry-level offerings like the Model 3.

Economies of scale are helpful here too, since larger companies can spend more on research and development to develop new battery chemistries.

Tesla and China enjoy battery cost advantages

I’m focusing on Tesla because it has arguably done more than any other company to drive down battery prices. According to BloombergNEF, Tesla controls 24 percent of the global market for battery electric vehicles. Tesla hasn’t shared its exact battery costs with BloombergNEF, but the group estimates Tesla spends $112 per kWh—15 percent below the industry average of $132.

Of course other companies are pursuing similar strategies: building larger factories to take advantage of economies of scale, developing new battery chemistries, and seeking volume discounts from their suppliers.

Beyond Tesla, industry leadership is centered in China. “The volume-weighted average and the spread tends to be higher outside of China,” the report says. “This reflects the relative immaturity of these markets.”

BloombergNEF estimates that the average battery customer in China pays $111 per kWh, compared to $154 in North America and $176 in Europe.

So does demand make prices go up or down?

Eagle-eyed readers may have noticed a tension in my explanation so far. On the one hand, I’ve portrayed rising battery demand as a major factor in falling battery prices. On the other hand, I’ve noted that rising commodity prices have pushed up battery costs. But surely rising commodity prices are due, at least in part, to strong demand for batteries.

So which is it? Does strong demand make batteries more or less expensive?

This largely depends on how much advance warning the industry has about rising demand.

It takes a few years to build a battery factory—or to set up a cobalt mine for that matter. Companies are reluctant to do this unless they’re confident there will be enough demand to allow them to recoup their investment. If they build a battery factory and can’t find enough customers, they could lose a lot of money.

For example, Tesla took a big risk when it broke ground on its Nevada Gigafactory in 2014. Tesla (and Panasonic) planned to spend billions of dollars on the project. If Tesla’s car business hadn’t grown fast enough to take advantage of the factory’s massive capacity, a lot of that money would have been wasted.

Indeed, this is one big reason suppliers are willing to give big discounts to major customers who sign long-term contracts. If a supplier can lock in a few big customers, it greatly reduces the risk of getting stuck with expensive, under-utilized facilities. The more customer commitments a company has, the safer it is borrow and spend on adding manufacturing capacity, and the more quickly the company can grow.

Obviously the last couple of years have not been like that. In 2020, the pandemic disrupted supply chains around the world. Many automakers cut back production—both due to health concerns for their workers and because they feared demand for cars would plummet. But then governments stepped up with massive stimulus packages, and the world suddenly had the opposite problem: soaring demand that strained manufacturing capacity for cars, batteries, and a lot of other products. It’s not surprising the battery industry was caught flat-footed.

But today's high commodity prices are likely to be a temporary problem. As pandemic-related volatility recedes, battery manufacturers should get a better sense for whether the high demand of 2021 is temporary or permanent. If it’s permanent, they should gain the confidence to invest in larger-scale manufacturing facilities. The same is true of upstream suppliers. If commodity prices stay elevated, for example, mining companies will invest in expanded capacity.

Subsidies and mandates can speed up price declines

The need for predictability is one reason that open-ended renewable energy subsidies are valuable. For example, Tesla benefitted a lot from the $7,500 tax credit the federal government gives to customers of the first 200,000 battery electric cars a company makes. The credit expanded the potential market for Tesla vehicles, making it easier for Tesla to raise money and to sign long-term contacts with suppliers.

Crucially, Tesla knew years in advance that its customers would be eligible for this credit. If the government handed out green energy subsidies on an annual, discretionary basis, the impact per dollar wouldn’t have been as positive.

Similarly, back in 2013, California’s public utilities commission mandated that utilities add 1.3 gigawatts of energy storage to their electric grids by the end of the 2010s. Setting targets like this well in advance encourages battery manufacturers to invest in capacity upgrades, knowing that battery demand is guaranteed to grow over time. The long-term result: cheaper batteries for everyone.

There’s still room for governments to do more of this. I’ve written before about proposed legislation to make the electric vehicle tax credit more generous. The same bill would also create a new tax credit for energy storage.

Meanwhile, a number of countries have pledged to achieve carbon neutrality in the coming decades, with 2040 and 2050 as popular target dates. Interestingly, BloombergNEF’s baseline forecast does not assume that countries will actually reach these targets.

But the researchers also present an alternative scenario where countries do hit their targets. That would require even more battery production. In this case, greater economies of scale would push battery pack prices down to $88 per kWh by 2024 (compared to $94 in the baseline scenario) and $52 per kWh by 2030 (compared to $59 in the baseline scenario).

In short, it's much cheaper for the world to decarbonize together than for any single country to do it alone. And doing it quickly might prove surprisingly affordable.

Full Stack Economic is supported by readers. If you are enjoying the newsletter, please consider becoming a paying subscriber.