Why low-paid workers have enjoyed a long wage boom

Why low-paid workers have enjoyed a long wage boom

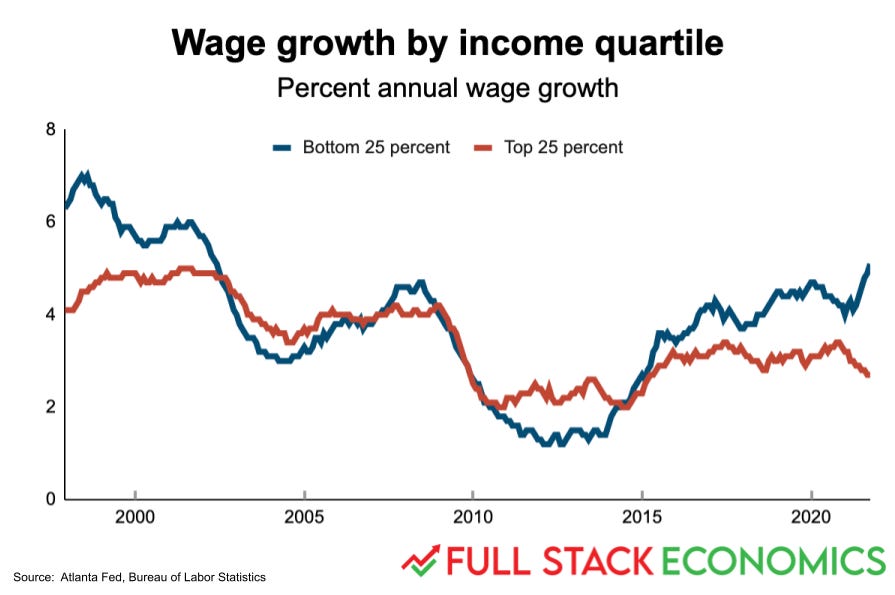

Booms and busts affect low-wage workers the most.

Over the last six years, wages for the bottom 25 percent of workers have risen at an average annual rate of 4.3 percent. Inflation averaged 2.5 percent over the same period, so their inflation-adjusted wages have been growing at 1.8 percent annually. This is the longest period of strong wage growth for low-paid workers since the dot-com era.

This is shown in the chart below, which was was inspired by the economics writer Joseph Politano (subscribe to his newsletter!) and is based on data from the Federal Reserve Bank of Atlanta. It illustrates an important principle of modern economies: workers at the bottom of the wage scale are affected more strongly by boom-and-bust cycles than those higher up.

When demand is soaring—as it was in 1999 and again in 2019—businesses want to hire every worker they can. That gives marginalized workers bargaining power and opportunities to move up the income ladder. When recessions hit, on the other hand, lower-paid workers are often the first to be let go. The ones who manage to hold on to their jobs have little bargaining power. As a result, their wages fall further behind. This happened from 2002 to 2005 and again between 2009 and 2013.

This insight has informed President Joe Biden’s economic agenda. In a May speech, Biden argued that full employment could provide “more options and opportunities for workers—including Black, Hispanic workers, Asian American workers, women—who’ve been left behind in previous economic recoveries when the labor market never tightened up enough.”

But while Biden has made full employment a priority for his economic team, he can’t claim all—or even most—of the credit for rising wages. As the chart above shows, labor markets tightened late in the Obama administration and stayed tight throughout the Trump years.

Since March 2020, the federal government has used a combination of lavish stimulus spending and loose monetary policy to ensure the pandemic didn’t throw the US economy off track. The policy worked a little too well, producing so much demand that inflation shot up to 6.2 percent. But while inflation is a real concern, we shouldn't lose sight of the benefits of these dovish policies: they've put a lot of money into the pockets of the workers who need it most.

Now the Fed is planning to tighten monetary policy to bring inflation back under control. The trick will be to avoid tightening so much that it tips the US into a recession—a recession that would likely put an end to strong wage growth at the lower rungs of the economic ladder.

Large retailers pushed wages higher

One of Democrats’ favorite ways to help low-wage workers is to raise the minimum wage. Democrats passed a minimum wage hike shortly after taking control of Congress in 2007, and they hoped to do so again after their victories in the 2020 election. But they’ve been unable to overcome a Republican filibuster, leaving the national minimum wage stuck at $7.25 for more than a decade.

Luckily, a strong labor market has forced most employers to give most low-wage workers raises even though they’re not legally required to do so.

As far back as 2015, I wrote about how tightening labor markets were putting upward pressure on wages. At the time, restaurants in a number of cities were struggling to recruit chefs and cooks. There were nationwide shortages of truck drivers. The construction industry has had a particular challenge finding enough workers because many construction workers who lost their jobs during the Great Recession left the construction industry altogether.

In January 2018, CNN reported on a Federal Reserve Survey that “found labor shortages all over the country. And more businesses said they had no choice but to pay more to attract and keep the workers they want.”

In recent years, large retailers have helped to set the pace for low-end wage hikes. In 2018, Walmart announced it would hike its minimum pay to $11 per hour. Target raised its minimum to $13 an hour in 2019. Costco set a $16 per hour minimum earlier this year.

Amazon has been even more aggressive. In 2018, the online retailer upped its national minimum wage to $15 per hour. In September of this year, Amazon said it was raising its average starting wage to $18 per hour.

These wage hikes didn’t just raise the incomes of hundreds of thousands of people who work for these specific retailers. A recent study by economists Ellora Derenoncourt, Clemens Noelke, and David Weil examined how wage hikes by these large retailers affected the broader labor market. They analyzed a large database of online job postings to see how other employers responded to a wage announcement by a giant like Amazon. They found that when Amazon raised its wages by 10 percent in a particular metropolitan area, it caused other employers in the same region to raise their own wages by an average of 2.6 percent.

So when an Amazon warehouse starts offering $18 per hour to new workers, it doesn’t quite set an $18 wage floor for other companies in the same town. But it does exert significant pressure on nearby employers, leading to raises for lots of workers who don’t work at Amazon.

The inflation conundrum

Of course, executives at these retail giants weren’t suddenly overcome with compassion for their workers. They boosted pay because they felt it was necessary to attract and retain a large workforce. That was made necessary by the tight labor market conditions of the late Obama and Trump years.

Dovish monetary and fiscal policies helped to sustain that boom. These included the tax cuts enacted by Republicans in 2017 and a series of Federal Reserve interest rate cuts that began in mid-2019. These were followed by much more aggressive stimulus efforts in 2020 and 2021, with the Fed slashing short-term interest rates to zero and Congress pushing out trillions of dollars in stimulus money. With so much cash sloshing around the economy, it was almost inevitable that consumer spending would rise, businesses would expand, and demand for workers would outstrip supply.

Of course, there’s a downside to excessive stimulus. If spending outstrips the economy’s productive capacity, the result is inflation. Inflation erodes the real value of workers’ paychecks. So even if policymakers engineer a large increase in nominal wages, that won’t necessarily mean workers get more spending power.

Before the pandemic, US policymakers struck a good balance. The wages of low-earning workers were growing at more than 4 percent per year, while average inflation was just below the Fed’s 2 percent target. So the workers’ real wages grew at more than 2 percent per year between 2015 and 2020.

The last year hasn’t been as good for workers in the bottom 25 percent of the wage distribution. Nominal wages grew by 5.1 percent, but the inflation rate was even higher at 6.2 percent. That means the real value of low-wage workers’ paychecks actually dropped by about one percent.

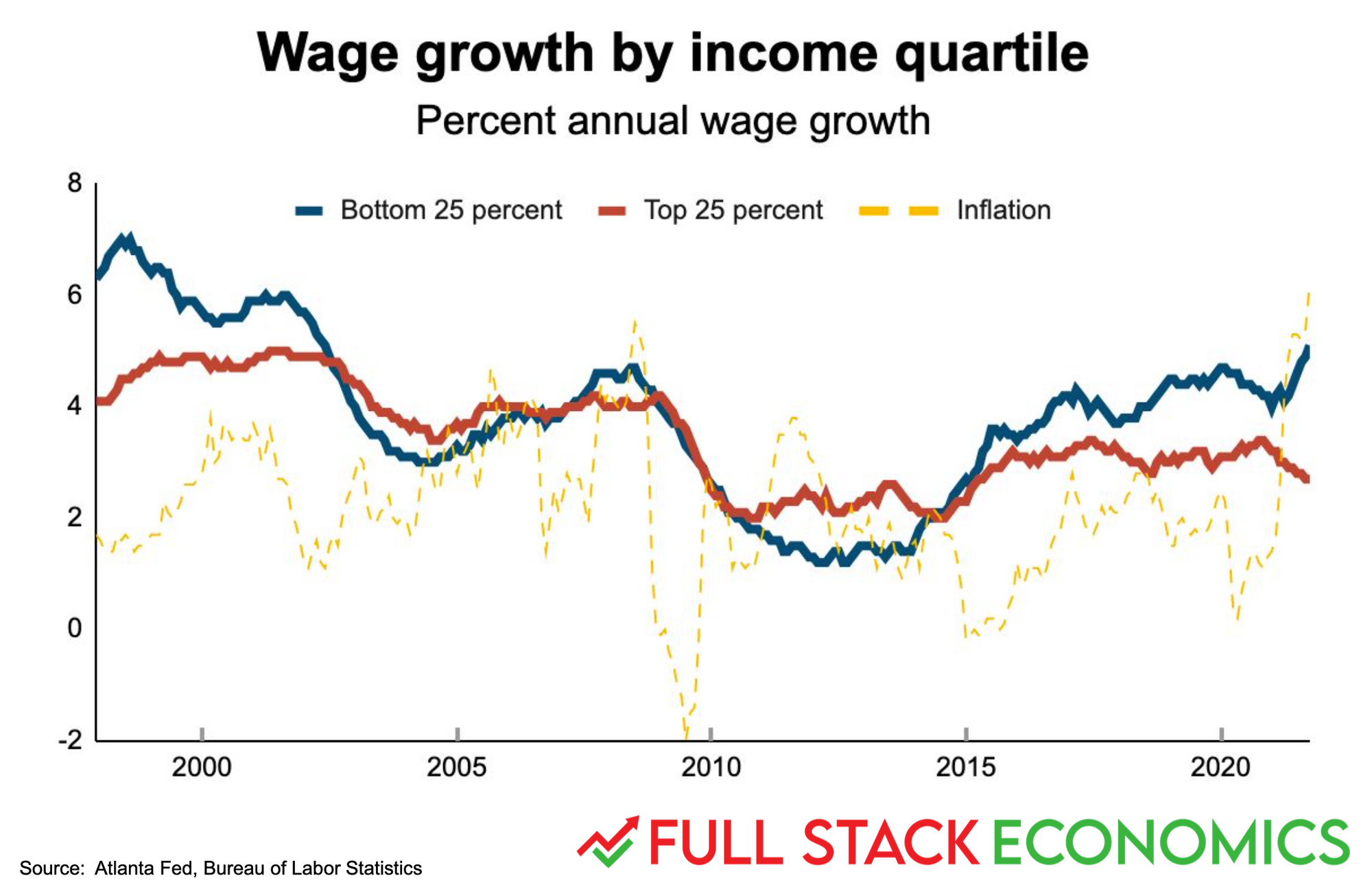

But we shouldn’t panic yet. Here I've added the inflation rate to the previous wage growth chart.

As you can see, the inflation rate bounces around a lot, driven by volatile categories like food and energy. But most of the time the inflation rate is lower than the wage growth rate. Wages tend to be a lagging indicator, so today's extremely tight labor market may set the stage for workers to get raises over the next year or two.

The next few months will be a bit of a high-wire act for the Fed. If the central bank tightens monetary policy too slowly, then we might see inflation continue to rise. In the worst-case scenario that could lead to a repeat of the 1970s. In this scenario, the real value of workers’ paychecks might not rise very much even if they get big nominal raises.

On the other hand, if the Fed over-reacts to the threat of inflation, that could tip the economy into a recession. And as we’ve seen, recessions are especially bad for low-income workers.

But there should be a happy medium in between: one that brings the inflation rate back down to around 2 percent without triggering a recession. If the Fed can manage that, it will be good news for low income workers, who could see several more years of wage growth well in excess of inflation.