Inflation the last two years was mainly about demand, not supply

A new paper from the Roosevelt Institute makes a weak case for the supply-shock view.

In recent months, inflation hawks have argued that inflation has been driven largely by excessive aggregate demand. This argument implies that Joe Biden’s March 2021 American Rescue Plan was too big, that the Federal Reserve should have started raising interest rates earlier, and—perhaps—that the Fed’s current campaign of aggressive interest rate hikes is justified.

But a recent paper from the Roosevelt Institute says that this is nonsense. The paper is co-authored by Nobel prize-winning economist Joseph Stiglitz and Roosevelt’s Ira Regmi, and it argues that the inflation of the last two years has not been driven by fiscal or monetary stimulus. Rather, they blame the war in Ukraine and the aftershocks of the COVID-19 pandemic.

A reader emailed me to ask what I thought of this paper. In a nutshell, I didn’t find it very persuasive. It’s definitely true that some of the inflation of the last year is due to supply chain disruptions. At a minimum, the war in Ukraine undeniably pushed up energy costs.

Gasoline prices rose by 60 percent between June 2021 and the peak of gasoline prices in June 2022. With gasoline prices accounting for about four percent of the average household’s budget, this meant that gasoline alone contributed something like 2.4 percentage points of the 9.1 percent annual inflation rate for June 2022. Inflation absolutely would not have soared so high last year if the war in Ukraine had not pushed energy prices up so much.

But core inflation—a measure that excludes volatile food and energy prices—was still 5.9 percent in June 2022. That’s way above the Fed’s 2 percent target. So this wasn’t the only factor driving high inflation—or even the main one.

Pandemic-related demand shifts contributed to inflation

I think Stiglitz and Regmi were correct to identify pandemic-related shifts in demand as a significant factor in the inflation of the last two years.

For example, in 2020 people went to fewer exercise classes and bought more exercise bikes. Demand for exercise bikes outstripped available supply, so prices soared. But there wasn’t a symmetrical decline in the prices of gyms and yoga studios. So, averaging across these two categories, prices rose as a result of shifting consumption patterns.

Stiglitz and Regmi argue that dynamics like this were a major factor pushing up prices over the last two years. Another example is in real estate. In 2020, demand collapsed for commercial real estate, especially in big cities. But demand soared for housing in certain parts of the country. Again, residential landlords facing high demand tended to raise their rents, while commercial landlords facing falling demand were less likely to cut their rents. So average rents across the economy rose.

The pandemic also caused some big shifts in the pattern of spending across time. In 2020 and early 2021, a lot of people cut back spending on certain categories and saved the money instead. As the economy started to open up in the second half of 2021, they started to spend down those savings, temporarily spending at a faster rate than the pre-COVID trend.

I think that’s a fine description of what happened in 2021, but I’m not sure I’d draw the same conclusion from this as the Roosevelt authors do. The authors say that policymakers should not have worried about these inflationary pressures, since they were likely to be temporary.

But I don’t think that’s right. A big reason Democrats passed the American Rescue Plan in 2021 was concern that there wouldn’t be enough spending to help the economy recover rapidly from the 2020 COVID recession. And to be fair, I thought this was a reasonable fear at the time.

But in hindsight, it’s clear that much of this spending was unnecessary and probably counterproductive. Consumers were going to spend a lot of money on televisions and furniture in 2021 regardless of what Congress did. If Congress had passed a smaller American Rescue Plan, consumers would have spent less, shortages would have been less severe and prices would not have risen so much.

It doesn’t really matter whether the stimulus spending was the original cause of the 2021 spending binge. Putting extra money in people’s pockets made it worse.

Supply chain problems were overrated

Inflation hawks say that inflation rose in 2021 because Congress and the Fed put too much money in consumers’ pockets. This is known in economics jargon as a demand shock. Doves like Stiglitz and Regmi counter that it happened because the pandemic temporarily reduced the nation’s productive capacity, known as a supply shock.

Here I think the Roosevelt report’s claims are just not backed up by the evidence. Here is the closest they come to empirical support for this claim:

A major explanation for these price increases is the idiosyncratic supply chain factors associated with the disruptions prompted by the pandemic shutdowns and subsequent reopenings. The Federal Reserve Bank of New York’s Global Supply Chain Pressure Index (GSCPI), which integrates various indices that analyze delivery times, backlogs, and inventories to assess supply chain pressures, shows that the sustained and frequent problems are much larger in magnitude compared to historic trends.

The problem with this argument is that demand shocks create supply chain problems too. If people start ordering a lot more stuff, that’s going to create shortages and expose supply-chain bottlenecks. So the fact that supply chains have been struggling to keep up with demand tells us nothing about whether that’s because demand is abnormally strong or supply is abnormally weak.

The way to tell the difference is by looking at the quantities of stuff being produced and consumed. When inflation is caused by a supply shock, we should see economic output running below historic norms. Whereas if inflation is driven by demand, then the economy should be producing at or above historic levels. Check out this chart for example:

In the spring of 2020, spending both goods and services briefly fell below 2019 levels. But then durable goods spending soared far above pre-pandemic levels. In November 2022, the most recent month for which we have data, durable goods spending was still 16 percent above the pre-pandemic trend. Services spending also recovered from the early 2020 lows, but it remains about 3 percent below trend.

The blue line on this chart just isn’t consistent with a supply-shock explanation for inflation. Durable goods inflation happened because demand for durable goods soared and suppliers couldn’t keep up. That’s a demand shock.

The red line is superficially more consistent with the Stiglitz/Regmi thesis. The pandemic certainly forced the closure of many bars, restaurants, gyms, concert venues, and the like. But as Stiglitz and Regmi note in their paper, the pandemic also crushed demand for many of these same services. So it’s not clear how much of the reduction in services spending is due to lower demand versus lower supply.

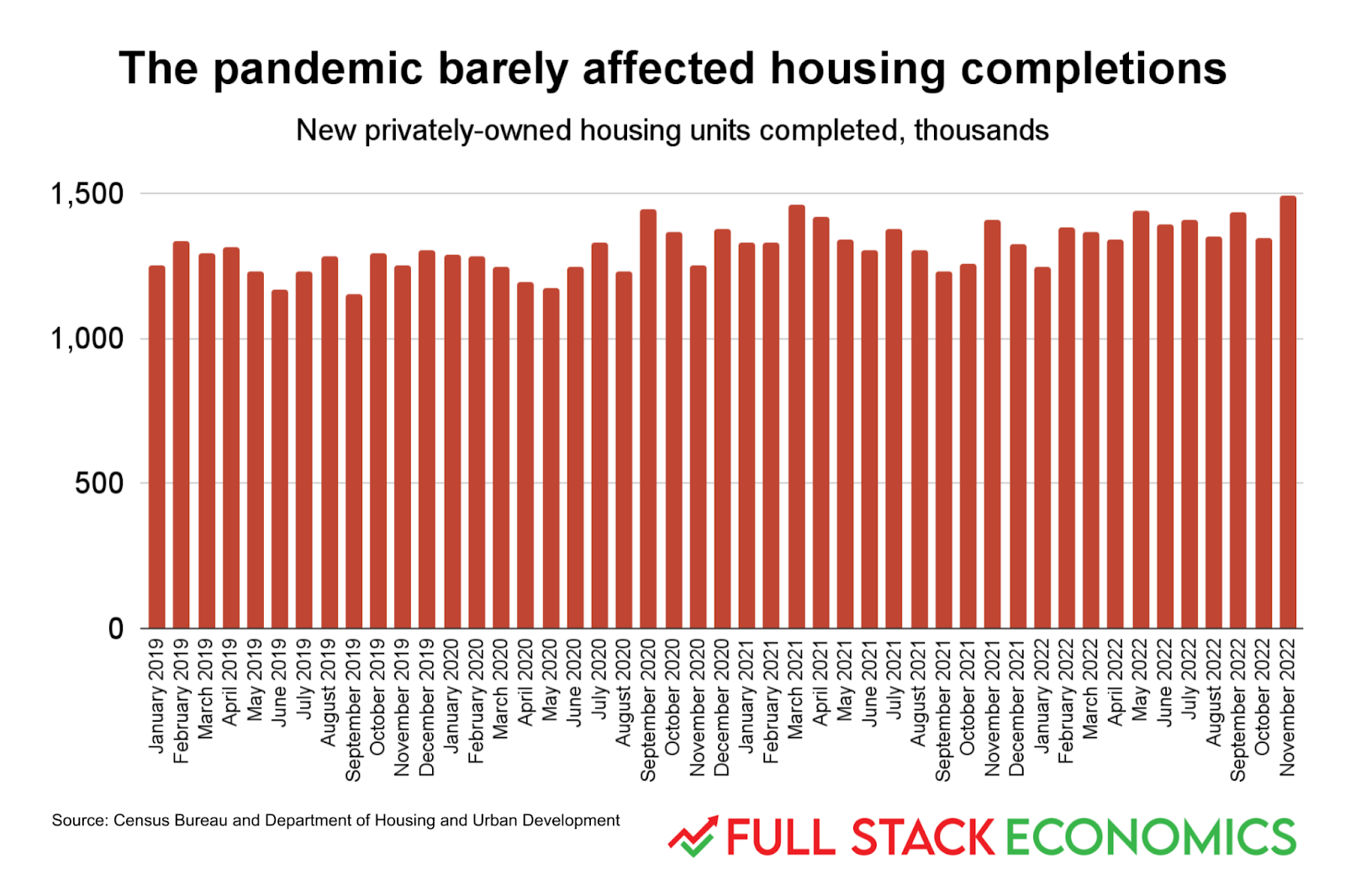

One of the biggest components of that red services line is housing. Did the pandemic disrupt the “supply chain” for housing? In a word, no:

The pandemic’s impact on housing production is so small that it’s difficult to even see on the chart. New home completions declined by about 9 percent between February and May 2020, but then housing completions set a new record in September. The US produced more housing units in 2020 than in 2019, and then more in 2021 than in 2020. So the soaring housing prices we saw in 2021 were clearly the result of surging demand, not pandemic-related problems with the housing supply chain.

The most commonly discussed supply chain problem concerns the automotive industry, which really has produced fewer cars since 2020 than they did in the late 2010s. But even here the conventional explanation isn’t quite right.

It’s true that car companies have been hamstrung by a shortage of computer chips. But the reason isn’t that the pandemic hampered the production of computer chips generally. To the contrary, the semiconductor industry shipped a record number of chips in 2021.

The problem for automakers is that in the early months of the pandemic they panicked and canceled a bunch of chip orders. Chipmakers re-allocated this spare capacity to other customers, and so when the economy rebounded in late 2020 and early 2021, carmakers found themselves at the end of long waiting lists for new chips, precisely because demand was surging for a wide range of durable goods.

Overall, consumers bought more durable goods than ever in 2021 and early 2022. Which makes it hard to believe that the inflation of that period was caused primarily by supply-chain problems.

While I’m fairly confident that Stiglitz and Regmi’s explanation for past inflation is wrong, I don’t necessarily think they’re wrong that the Fed is tightening too rapidly. Monetary policy was clearly too loose a year ago, and we clearly needed significant interest rate hikes last year to bring inflation under control. But inflation is now coming down, and it’s possible the Fed has now raised rates enough—or even too much—to bring inflation under control.

The question is which direction is it worse to overshoot? Drive the economy into a recession, or have high inflation for a longer duration of time?

I have a maybe related question. Inflation has been quite low for a while. Wealth concentration has also been quite high for a while. Is there any way to tell if the two are related? If you give a billionaire a billion dollars, his spending is not likely to increase substantially. If you give a million people in poverty each a thousand dollars, all of their spending will increase. The various COVID stimulus bills have definitely been closer to the latter and can explain the higher inflation. Does the wealth concentration help explain the lower inflation from before?

Nice analysis. I think the word "idiosyncratic supply chain factors" in your snippet from Stiglitz-Regmi speaks volumes. It amounts to a this-time-is-different argument, which you demolish quite nicely.

As to your conclusion, none of us - not the Fed, not macro- or policy-economic establishment, not the markets - know how much Fed action is enough. If you buy the theory that inflation expectations are the inflation driver, it seems like the Fed ought to pause and see what comes down. If you take a Phillips curve or labor market approach, the economy must seem stubbornly resistant to fiscal tightening, it seems like they have "more work to do". Inflation-fighting sucks.